What to Expect During a VA Appraisal (And What Happens If It Comes in Low)

If you're using a VA loan to buy a home, one key milestone is the VA appraisal. It’s not just about value. It’s about making sure the home is safe, sound, and move-in ready — all based on the VA’s rules and timelines.

This guide walks you through what appraisers are looking for, how the Tidewater Initiative works, what happens if the value comes in low, and how long it should take in your state.

What Does a VA Appraiser Look For?

VA appraisers are licensed professionals chosen by the Department of Veterans Affairs. You can’t choose your own, and their job is twofold:

1. Estimate Fair Market Value

They compare your home to recently sold, similar properties to make sure the home is worth the contract price.

2. Verify Minimum Property Requirements (MPRs)

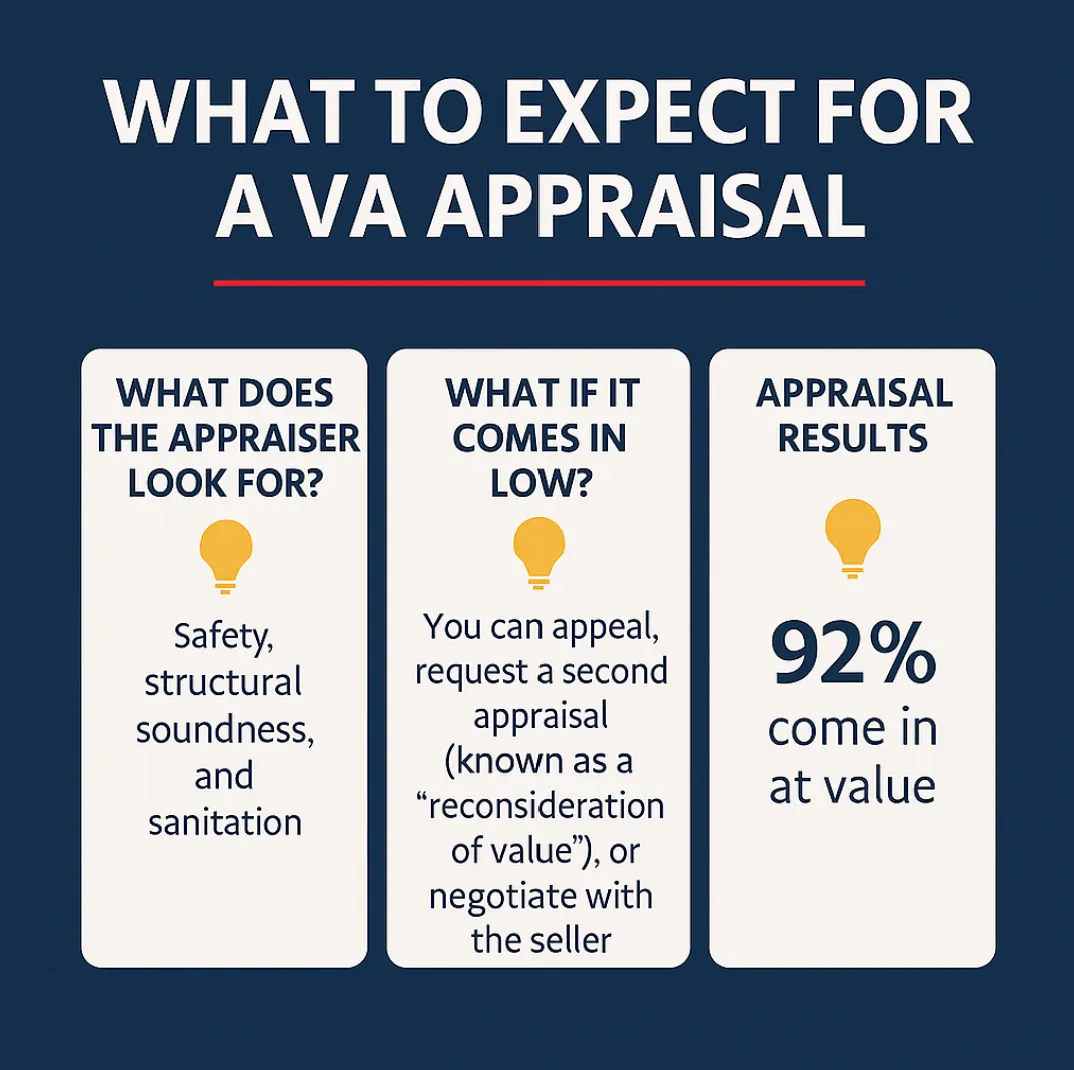

The VA wants you to buy a home that is safe, sanitary, and structurally sound. The appraiser checks for:

Working electric, plumbing, and heating systems

A roof in good shape with no active leaks

No exposed wiring, broken stairs, or peeling lead-based paint

Clean water and a safe sewage system

No major foundation or structural damage

Safe access from a public or all-weather road

No obvious hazards such as pest infestations

Note: The VA appraisal is not a replacement for a home inspection. You should still get a separate inspection to uncover issues that don’t affect loan eligibility but could impact your comfort and wallet.

What Is the VA Tidewater Initiative?

Tidewater is the VA’s early warning system for low appraisals. If the appraiser believes the value may come in below the purchase price, they don’t finalize the report immediately.

Instead, they notify the lender that Tidewater has been initiated. The lender then has 48 hours to submit additional comparable sales that may support the value.

💡 If you’re working with a VA-experienced agent and lender, they’ll be ready to respond quickly to protect your offer.

Once comps are reviewed, the appraiser finalizes the report. Tidewater does not guarantee a higher value, but it gives your team a fair chance to justify your offer.

What If the Appraisal Comes in Low?

Even after Tidewater, the value might still fall short. The good news is the VA loan program gives you options.

Your choices include:

Renegotiate the price with the seller

Request a Reconsideration of Value (ROV) with stronger comps

Pay the difference in cash, if you choose to

Walk away — you’re not required to proceed if the value doesn’t support the loan

The ROV process is separate from Tidewater and allows you to appeal the final appraised value through your lender.

How Often Do VA Appraisals Come in Low?

According to Veterans United and VA lending data:

92% of VA appraisals come in at or above the purchase price

Only 8% fall short, and many of those are resolved through Tidewater or an ROV

That means most VA buyers don’t run into problems with value.

How Long Does a VA Appraisal Take?

The VA sets timelines and fee caps by state. Here are the current examples for Idaho, Utah, and Florida:

StateMax Turn TimeTypical FeeIdaho10 business days$750 – $800Utah10 business days$725 – $775Florida7–10 business days$675 – $775

These timelines apply to single-family homes in most counties. Complex properties, rural areas, and manufactured homes may take longer.

For the full VA fee and turn time chart by state, visit:

VA Appraisal Fee Schedule

Final Advice

Always get a home inspection. The VA appraisal is not meant to protect you from every issue.

If you hear the word “Tidewater,” act fast and lean on your real estate team.

If repairs are required, the seller typically must complete them before closing.

Don’t panic if the value comes in low. You’ve got options — and you’re protected.