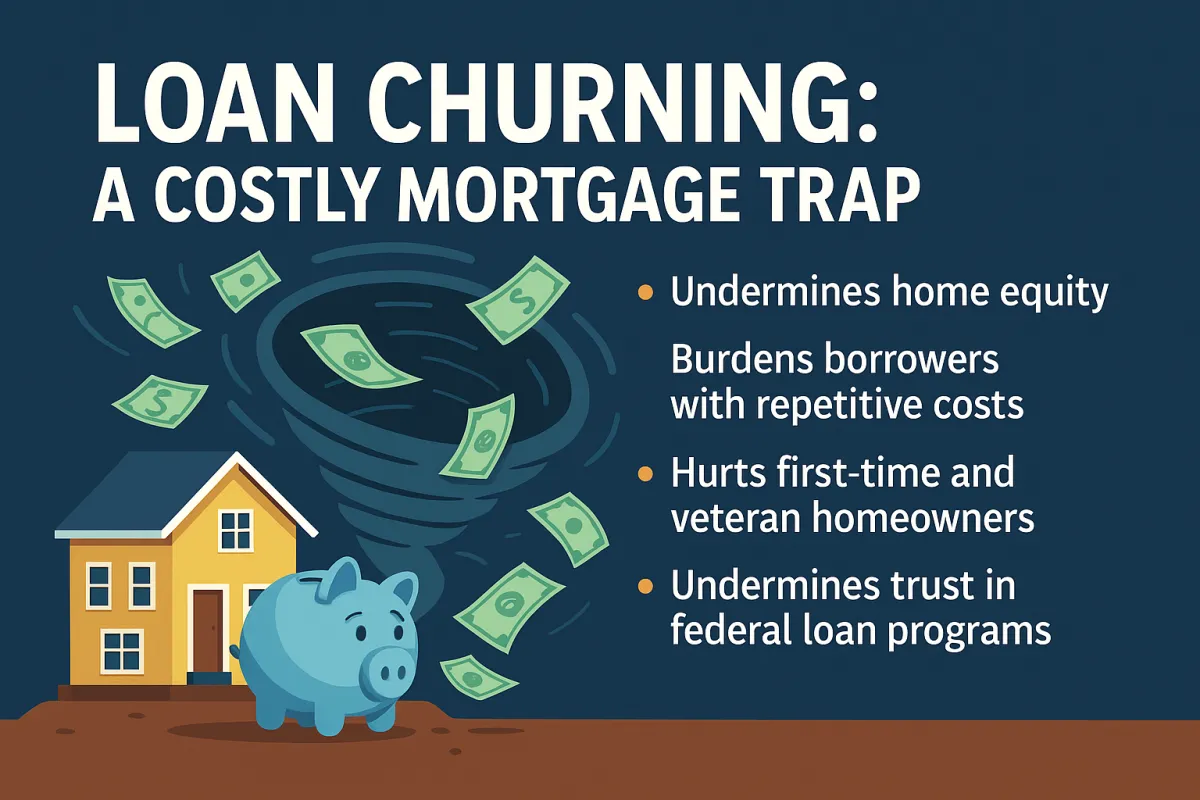

Loan Churning: A Costly Mortgage Trap

Loan churning, sometimes called “loan flipping,” happens when borrowers are convinced to refinance repeatedly without any real financial benefit. Every time a loan is refinanced, new closing costs and fees are added, often rolled into the loan balance. This slowly drains home equity and increases the total cost of the mortgage. Even a slightly lower interest rate usually does not offset the extra costs.

Why Churning is Dangerous

Equity erosion: Adding closing costs to the loan increases the principal balance, which reduces the homeowner’s equity and can make it harder to refinance or sell later.

Extra fees: Each refinance means paying another round of closing costs, prepayment penalties, and lender fees, which quickly add up.

Investor fallout: When loans are refinanced too quickly, the investors who buy mortgage-backed securities earn less on their investment. This makes them less willing to invest in programs like VA, FHA, and USDA, which can drive up borrowing costs for everyone.

VA, FHA, and First-Time Homebuyers: Why They Were Hit Hardest

Veterans and VA Loans

Veterans were a frequent target for churning schemes. Some lenders would encourage them to switch from adjustable-rate mortgages (ARMs) to fixed-rate loans soon after closing. These offers often came with promises of skipping a couple of payments or getting cash back from escrow refunds. In reality, the true costs were hidden in the new loan terms. The problem became so widespread that the VA introduced a rule requiring borrowers to wait 210 days after their first payment before refinancing.

How FHA Borrowers Were Affected

While VA loans got the most attention, FHA loans—commonly used by first-time buyers—were also impacted. FHA, USDA, and VA programs all saw the negative effects of rapid refinancing. This weakened confidence in these government-backed mortgages and made them more expensive. First-time buyers, who often choose FHA loans for the low down payment and flexible credit requirements, were especially vulnerable.

Broader Impact on Borrowers

Higher delinquency risk: Repeated refinancing often increased loan balances and extended terms, which made it harder for some homeowners to keep up with payments. FHA borrowers, in particular, saw rising delinquency rates during these periods.

Market distortion: High volumes of early refinances sped up prepayment rates, disrupted the mortgage-backed securities market, and led to stricter lending rules and oversight.

The Fallout and Regulatory Response

Loan churning nearly destabilized Ginnie Mae–backed programs, which are a backbone for VA, FHA, and USDA loans. In response, the VA, FHA, CFPB, and Congress implemented stricter rules. These included mandatory waiting periods, clearer disclosures, and tougher penalties for lenders engaging in abusive practices.

Things to Remember

Loan churning is not just an inconvenience. It is harmful because it:

Reduces your home equity

Adds repetitive and unnecessary costs

Damages trust in federal loan programs

Disproportionately impacts first-time buyers and veterans

What Homeowners Can Do

Avoid refinancing unless it will truly improve your financial situation.

Calculate all costs, rate changes, and term adjustments before agreeing to a refinance.

Work with lenders who are transparent and have your best interests in mind.

Protect your equity, your wallet, and your peace of mind by staying informed and cautious.